7 Easy Facts About Mortgage Investment Corporation Explained

7 Easy Facts About Mortgage Investment Corporation Explained

Blog Article

What Does Mortgage Investment Corporation Do?

Table of ContentsThe smart Trick of Mortgage Investment Corporation That Nobody is DiscussingThe smart Trick of Mortgage Investment Corporation That Nobody is Talking AboutA Biased View of Mortgage Investment Corporation

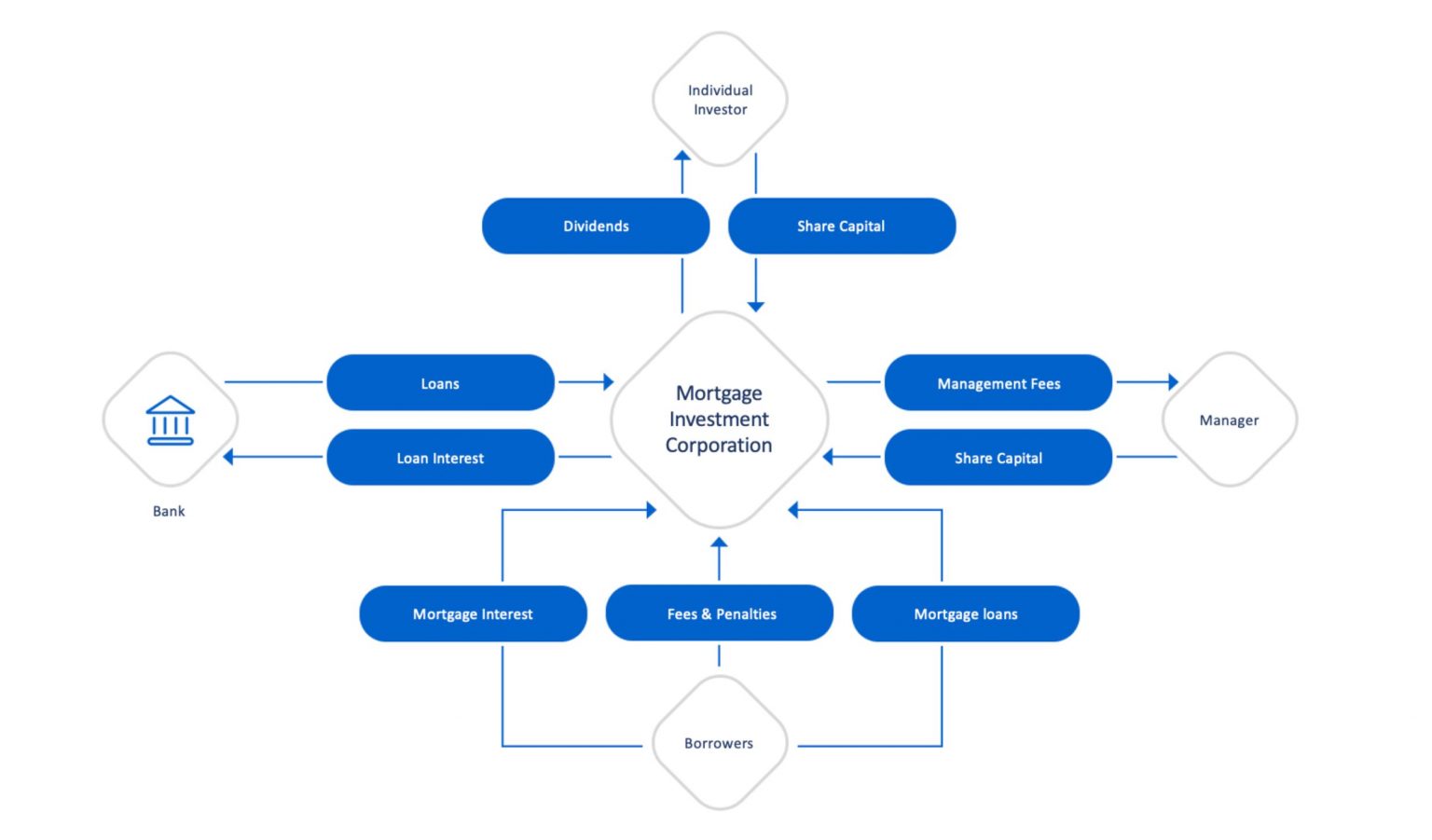

This indicates that capitalists can delight in a consistent stream of capital without having to proactively manage their financial investment profile or worry regarding market variations. In addition, as long as borrowers pay their mortgage on schedule, earnings from MIC investments will stay steady. At the exact same time, when a consumer ceases paying on time, financiers can count on the knowledgeable team at the MIC to deal with that situation and see the lending with the departure process, whatever that looks like.

As necessary, the objective is for investors to be able to gain access to stable, lasting capital generated by a large capital base. Dividends received by investors of a MIC are usually identified as passion revenue for objectives of the ITA. Resources gains recognized by a financier on the shares of a MIC are typically subject to the regular therapy of funding gains under the ITA (i.e., in a lot of situations, taxed at one-half the rate of tax obligation on normal earnings).

While certain demands are kicked back till shortly after the end of the MIC's first financial year-end, the complying with standards have to generally be satisfied for a corporation to qualify for and preserve its condition as, a MIC: homeowner in Canada for purposes of the ITA and incorporated under the legislations of Canada or a district (unique rules put on companies included prior to June 18, 1971); just task is spending of funds of the firm and it does not take care of or create any kind of genuine or unmovable building; none of the residential property of the corporation includes financial debts possessing to the firm safeguarded on genuine or stationary home located outside Canada, debts possessing to the firm by non-resident individuals, except debts safeguarded on real or stationary home situated in Canada, shares of the resources supply of companies not resident in Canada, or actual or stationary home situated outdoors Canada, or any type of leasehold interest in such property; there are 20 or even more shareholders of the firm and no shareholder of the corporation (along with specific persons associated with the investor) owns, straight or indirectly, more than 25% of the released shares of any type of course of the funding stock of the MIC (specific "look-through" rules use in respect of trust funds and partnerships); owners of favored shares have a right, after payment of favored dividends and settlement of returns in a like amount per share to the owners of the usual shares, to individual pari passu with the holders of typical shares in any additional returns settlements; a minimum of 50% of the price amount of all property of the company is spent in: financial obligations secured by home loans, hypotecs or in any various other manner on official statement "homes" (as defined in the National Housing Act) or on property consisted of within a "real estate project" (as defined in the National Real Estate Act as it checked out on June 16, 1999); down payments in the records of the majority of Canadian banks or credit scores unions; and cash; the cost quantity to the corporation of all genuine or unmovable residential or commercial property, consisting of leasehold passions in such property (excluding specific quantities gotten by repossession or according to a debtor default) does not surpass 25% of the expense quantity of all its property; and it complies with the obligation limits under the ITA.

4 Simple Techniques For Mortgage Investment Corporation

Capital Structure Private MICs generally provided two classes of shares, typical and favored. Common shares are usually provided to MIC creators, supervisors and police officers. Typical Shares have voting legal rights, are normally not qualified to returns and have no redemption attribute yet get involved in the circulation of MIC properties after preferred shareholders get accrued but overdue rewards.

Preferred shares do not commonly have ballot legal rights, are redeemable at the choice of the holder, and in some circumstances, by the MIC. On ending up or liquidation of the MIC, liked shareholders are generally qualified to obtain the redemption value of each preferred share as well as any kind of stated but unpaid rewards.

One of the most typically counted on prospectus exceptions for personal MICs distributing safety and securities are the "accredited capitalist" exemption (the ""), the "offering memorandum" exemption (the "") and to a minimal degree, the "family, buddies and business affiliates" exemption (the "") (Mortgage Investment Corporation). Capitalists under the AI Exception are usually higher total assets financiers than those who might just satisfy the threshold to spend under the OM Exception (depending on the jurisdiction in Canada) and are most likely to invest greater amounts of capital

The Single Strategy To Use For Mortgage Investment Corporation

Investors under the OM Exemption normally have a reduced total assets than certified investors and depending upon the territory in Canada undergo caps respecting the amount of capital they can invest. In Ontario under the OM Exemption an "eligible investor" is able to invest up to $30,000, or $100,000 if such investor receives suitability guidance from a registrant, whereas a "non-eligible investor" can only invest up to $10,000.

Historically low rate of interest recently that has led Canadian financiers to progressively venture into the world of private home loan financial investment firms or MICs. These frameworks assure constant returns at a lot greater returns than traditional fixed earnings financial investments nowadays. However are they as look at this site well great to be real? Dustin Van Der Hout and James Cost of Richardson GMP in Toronto article source believe so.

Report this page